| ■ 영문 제목 : Advanced Driver Monitoring Systems Market Forecasts to 2032 – Global Analysis By Component (Camera Modules, Infrared Sensors, Steering Angle Sensors, Driver Monitoring ECUs, Illumination Units and Software Algorithms), Monitoring Type, Vehicle Type, Technology, End User, and By Geography | |

| ■ 상품 코드 : SMRC33075 ■ 조사/발행회사 : Stratistics MRC ■ 발행일 : 2026년 1월 ■ 페이지수 : 150 ■ 작성언어 : 영어 ■ 보고서 형태 : PDF ■ 납품 방식 : E메일 (주문 후 3영업일) ■ 조사대상 지역 : 글로벌 ■ 산업 분야 : 자동차 |

| Single User (1명 열람용) | USD4,150 ⇒환산₩5,810,000 | 견적의뢰/주문/질문 |

| Enterprise License (동일기업내 공유가능) | USD7,500 ⇒환산₩10,500,000 | 견적의뢰/주문/질문 |

|

※가격옵션 설명 - 납기는 즉일~2일소요됩니다. 3일이상 소요되는 경우는 별도표기 또는 연락드립니다. - 지불방법은 계좌이체/무통장입금 또는 카드결제입니다. |

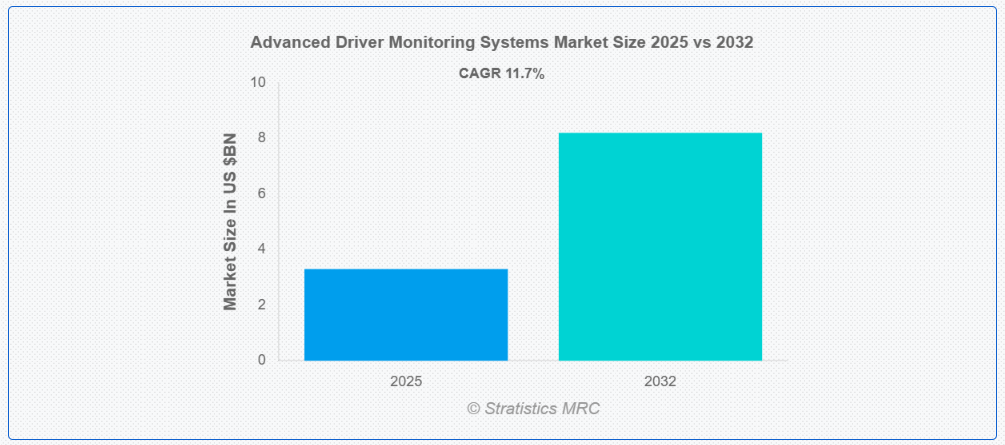

| Stratistics MRC에 따르면 글로벌 첨단 운전자 모니터링 시스템(ADMS) 시장은 2025년 약 33억 달러 규모로 추정되며, 2032년에는 82억 달러까지 성장해 예측 기간 동안 연평균 11.7%의 성장률을 기록할 전망이다. ADMS는 카메라, 센서, AI 알고리즘을 활용해 운전자의 시선, 머리 움직임, 표정, 조향 패턴 등을 분석함으로써 졸음, 주의 분산, 이상 상태를 감지하고 경고 또는 보정 조치를 제공하는 차량 내 안전 기술로, 자율·반자율 주행차와 플릿 관리, 규제 대응에서 핵심적인 역할을 한다. 시장 성장은 교통사고 증가와 완성차 업체의 안전 책임 강화로 인해 차량 안전에 대한 관심이 높아진 점이 주요 동인이다. 소비자들의 안전 및 프리미엄 기능에 대한 수요 확대와 반자율 주행 확산도 ADMS 도입을 가속화하고 있다. 반면 고성능 카메라, 적외선 센서, AI 분석 소프트웨어 및 ADAS와의 통합에 따른 높은 시스템 비용과 유지·검증 부담은 특히 가격 민감도가 높은 차급과 신흥 시장에서 도입을 제한하는 요인으로 작용한다. 각국 정부의 운전자 안전 관련 의무 규제는 중요한 성장 기회로 평가된다. 피로 및 주의 분산 사고를 줄이기 위한 법·제도 강화와 Euro NCAP 등 글로벌 안전 기준 확대로 ADMS의 기본 탑재가 확대되며, 장기적 수요 안정성과 기술 표준화, 완성차 업체와의 장기 계약 기회를 창출하고 있다. 반면 차량 내부 모니터링에 대한 개인정보 보호 우려와 소비자 거부감은 시장 확산에 위협 요인으로 작용할 수 있으며, 기능 제한이나 선택적 비활성화 요구로 시스템 효과가 약화될 가능성도 존재한다. 코로나19 팬데믹은 단기적으로 자동차 생산 및 공급망 차질로 시장에 부정적 영향을 주었으나, 이후 안전·자동화·비접촉 기술에 대한 관심이 높아지며 ADMS 수요는 빠르게 회복됐다. 장기적으로는 지능형 모빌리티 투자 확대와 함께 첨단 안전 시스템에 대한 필요성이 더욱 강화되었다. 구성요소 측면에서는 운전자 행동을 실시간으로 분석하는 핵심 역할을 수행하는 카메라 모듈이 가장 큰 비중을 차지할 것으로 전망되며, 적외선 이미징과 AI 비전 기술의 발전이 이를 뒷받침하고 있다. 기능별로는 피로 운전 사고에 대한 경각심이 커지면서 졸음 감지 부문이 가장 높은 성장률을 보일 것으로 예상되며, 상용차와 고급 승용차에서 채택이 빠르게 확대되고 있다. 지역별로는 아시아태평양이 높은 차량 생산량과 안전 기술 도입 확대, 중국·일본·한국을 중심으로 한 OEM 투자 증가에 힘입어 최대 시장이 될 전망이다. 반면 북미는 첨단 자동차 기술의 조기 도입, 엄격한 안전 규제, 반자율 주행차 확산을 바탕으로 가장 높은 성장률을 기록할 것으로 예상된다. 시장에는 다양한 글로벌 기업들이 참여하고 있으며, 전반적으로 첨단 센서 기술과 AI 기반 분석 역량을 중심으로 기술 고도화와 적용 영역 확대가 지속되고 있다. ADMS 시장은 규제 강화와 기술 발전, 안전에 대한 인식 제고를 배경으로 중장기적으로 견조한 성장세를 이어갈 것으로 전망된다. |

According to Stratistics MRC, the Global Advanced Driver Monitoring Systems Market is accounted for $3.3 billion in 2025 and is expected to reach $8.2 billion by 2032 growing at a CAGR of 11.7% during the forecast period. Advanced Driver Monitoring Systems (DMS) are in-vehicle technologies that use cameras, sensors, and AI algorithms to assess driver behavior, alertness, and compliance. They track eye movement, head position, facial expressions, and steering patterns to detect fatigue, distraction, or impairment. Widely adopted in automotive safety frameworks, DMS enhance road safety by issuing warnings or initiating corrective actions. They are critical for autonomous and semi-autonomous vehicles, fleet safety management, and regulatory compliance in modern transportation ecosystems.

Market Dynamics:

Driver:

Growing focus on vehicle safety

Growing emphasis on vehicle safety is a primary growth driver for the Advanced Driver Monitoring Systems market, fueled by rising road accident statistics and heightened OEM accountability. Automakers are increasingly integrating in-cabin sensing technologies to monitor driver alertness, gaze, and behavior in real time. Spurred by consumer demand for safer mobility and premium safety features, ADMS adoption is accelerating across passenger and commercial vehicles. The shift toward semi-autonomous driving further amplifies the need for robust driver state monitoring solutions.

Restraint:

High system integration costs

High system integration costs remain a significant restraint, particularly for cost-sensitive vehicle segments. Advanced Driver Monitoring Systems require sophisticated hardware, software algorithms, and seamless integration with existing vehicle electronics and ADAS platforms. Influenced by the need for high-performance cameras, infrared sensors, and AI-driven analytics, overall system costs increase substantially. For mass-market OEMs and emerging-market manufacturers, these expenses can limit large-scale deployment. Additionally, ongoing calibration, testing, and compliance costs further challenge profitability and slow adoption rates.

Opportunity:

Mandatory driver safety regulations

Mandatory driver safety regulations present a strong growth opportunity for the Advanced Driver Monitoring Systems market. Governments and regulatory bodies are increasingly mandating driver monitoring features to reduce accidents caused by fatigue and distraction. Propelled by initiatives such as Euro NCAP requirements and upcoming global safety norms, OEMs are compelled to integrate ADMS as standard equipment. This regulatory push creates long-term demand stability, encourages technological standardization, and opens opportunities for suppliers to secure long-term contracts with automotive manufacturers worldwide.

Threat:

Consumer resistance to in-cabin monitoring

Consumer resistance to in-cabin monitoring poses a notable threat to market expansion. Privacy concerns related to continuous video recording and data usage can negatively influence adoption, particularly in developed markets. Fueled by growing awareness around data security and personal privacy, some consumers perceive driver monitoring systems as intrusive. This skepticism can pressure OEMs to limit functionality or offer opt-out features, potentially reducing system effectiveness. Negative public perception and regulatory scrutiny over data handling may further restrain widespread acceptance.

Covid-19 Impact:

The COVID-19 pandemic had a mixed impact on the Advanced Driver Monitoring Systems market. Short-term disruptions in automotive production, semiconductor supply chains, and vehicle sales temporarily slowed market growth. However, post-pandemic recovery has been marked by renewed focus on vehicle safety, automation, and contactless technologies. Motivated by accelerated digital transformation and rising investments in intelligent mobility, ADMS adoption rebounded strongly. The pandemic ultimately reinforced long-term demand for advanced safety systems despite initial manufacturing and logistics challenges.

The camera modules segment is expected to be the largest during the forecast period

The camera modules segment is expected to account for the largest market share during the forecast period, resulting from its critical role in real-time driver behavior analysis. Camera-based solutions enable accurate detection of eye movement, facial expressions, and head position, making them central to ADMS functionality. Driven by continuous advancements in infrared imaging and AI-based vision processing, camera modules offer high reliability across lighting conditions. Their scalability and compatibility with multiple safety applications further strengthen segment dominance.

The drowsiness detection segment is expected to have the highest CAGR during the forecast period

Over the forecast period, the drowsiness detection segment is predicted to witness the highest growth rate, propelled by increasing awareness of fatigue-related accidents. Automotive regulators and OEMs are prioritizing technologies that can proactively identify early signs of driver fatigue. Spurred by advancements in biometric analytics and machine learning algorithms, drowsiness detection systems are becoming more accurate and responsive. Their growing adoption in long-haul commercial vehicles and premium passenger cars significantly contributes to the segment’s rapid CAGR.

Region with largest share:

During the forecast period, the Asia Pacific region is expected to hold the largest market share, attributed to high vehicle production volumes and rapid adoption of advanced safety technologies. Countries such as China, Japan, and South Korea are witnessing strong OEM investments in ADAS and driver monitoring solutions. Supported by expanding middle-class demand for safer vehicles and favorable government safety initiatives, the region offers a robust manufacturing ecosystem. Cost-effective component sourcing further enhances regional market leadership.

Region with highest CAGR:

Over the forecast period, the North America region is anticipated to exhibit the highest CAGR associated with early adoption of advanced automotive technologies and stringent safety regulations. The presence of leading OEMs, technology providers, and AI-driven mobility innovators accelerates ADMS deployment. Driven by rising consumer preference for premium safety features and increasing penetration of semi-autonomous vehicles, demand continues to surge. Additionally, strong regulatory emphasis on reducing distracted driving supports sustained, high-growth market momentum.

Key players in the market

Some of the key players in Advanced Driver Monitoring Systems Market include Siemens Energy AG, GE Vernova, Vestas Wind Systems A/S, ABB Ltd., Hitachi Energy Ltd., Schneider Electric SE, Prysmian Group, Nexans S.A., LS Cable & System Ltd., Sumitomo Electric Industries, Ltd., NKT A/S, Mitsubishi Electric Corporation, Eaton Corporation plc, Emerson Electric Co., and Ørsted A/S

Key Developments:

In October 2025, Siemens released its Infrastructure Transition Monitor 2025, highlighting AI-driven autonomous grid systems and digital infrastructure as critical enablers for resilient energy and mobility platforms, including driver monitoring integration.

In September 2025, GE Vernova partnered with EnergyHub to integrate GridOS® DERMS with advanced edge analytics, enabling real-time monitoring and predictive diagnostics for vehicle and driver behavior across distributed energy fleets.

In September 2025, Vestas and GE Vernova deployed advanced shaft speed sensors to enhance turbine reliability. These sensors, adapted for vehicular platforms, support rotational behavior tracking in driver monitoring systems.

Components Covered:

• Camera Modules

• Infrared Sensors

• Steering Angle Sensors

• Driver Monitoring ECUs

• Illumination Units

• Software Algorithms

Monitoring Types Covered:

• Drowsiness Detection

• Distraction Detection

• Gaze Tracking

• Head Pose Monitoring

• Emotion Recognition

Vehicle Types Covered:

• Passenger Vehicles

• Light Commercial Vehicles

• Heavy Commercial Vehicles

Technologies Covered:

• Computer Vision

• AI & Machine Learning

• Infrared Imaging

• Biometric Sensing

End Users Covered:

• Private Vehicle Owners

• Fleet Operators

• Ride-Hailing & Mobility Service Providers

• Logistics & Transportation Companies

• Public Transportation Authorities

Regions Covered:

• North America

o US

o Canada

o Mexico

• Europe

o Germany

o UK

o Italy

o France

o Spain

o Rest of Europe

• Asia Pacific

o Japan

o China

o India

o Australia

o New Zealand

o South Korea

o Rest of Asia Pacific

• South America

o Argentina

o Brazil

o Chile

o Rest of South America

• Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Rest of Middle East & Africa

1 Executive Summary 2 Preface 3 Market Trend Analysis 4 Porters Five Force Analysis 5 Global Advanced Driver Monitoring Systems Market, By Component 6 Global Advanced Driver Monitoring Systems Market, By Monitoring Type 7 Global Advanced Driver Monitoring Systems Market, By Vehicle Type 8 Global Advanced Driver Monitoring Systems Market, By Technology 9 Global Advanced Driver Monitoring Systems Market, By End User 10 Global Advanced Driver Monitoring Systems Market, By Geography 11 Key Developments 12 Company Profiling List of Tables Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above. |

| ※본 조사보고서 [세계의 첨단 운전자 모니터링 시스템 시장 전망 (2032년)] (코드 : SMRC33075) 판매에 관한 면책사항을 반드시 확인하세요. |

| ※본 조사보고서 [세계의 첨단 운전자 모니터링 시스템 시장 전망 (2032년)] 에 대해서 E메일 문의는 여기를 클릭하세요. |

※당 사이트에 없는 자료도 취급 가능한 경우가 많으니 문의 주세요!